and BIY customers. We have also invested in technology and personnel to support our stores. We believe that our investments in our business will continue to improve our customer value proposition, differentiating us and strengthening our competitive advantage.

We believe our strong financial results are a reflection of our consistent and disciplined culture of innovation and reinvestment, creating a differentiated business model in the hard surface flooring category, as evidenced by the following:

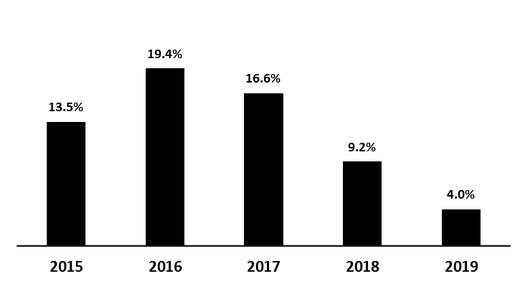

• | eleven years of comparable store sales growth averaging 13.8% per year (and averaging 12.5% per year for fiscal 2015 to fiscal 2019) with a 4.0% increase in fiscal 2019 compared to 9.2% for fiscal 2018; |

• | store base expansion from 57 warehouse-format stores at the end of fiscal 2015 to 120 warehouse-format stores at the end of fiscal 2019, representing a compound annual growth rate (“CAGR”) of 20.5%; we added 20 warehouse-format stores during fiscal 2019, which was a 20.0% growth in units compared to fiscal 2018; |

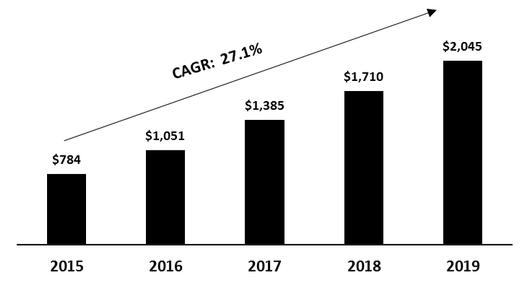

• | total net sales growth from $784.0 million to $2.05 billion from fiscal 2015 to fiscal 2019, representing a CAGR of 27.1%; |

• | net income growth from $26.8 million to $150.6 million from fiscal 2015 to fiscal 2019, representing a CAGR of 54.0%; |

• | Adjusted EBITDA growth from $72.9 million to $242.6 million from fiscal 2015 to fiscal 2019, representing a CAGR of 35.1%, which includes significant investments in our sourcing and distribution network, integrated IT systems, and corporate overhead to support our future growth. Adjusted EBITDA was $242.6 million for fiscal 2019, an increase of 26.4% over fiscal 2018. Adjusted EBITDA is a non-GAAP (as defined below) financial measure. For a reconciliation of net income to Adjusted EBITDA, see Item 6 “Selected Financial Data.” |

Net Sales (in millions)

| Comparable Store Sales Growth

|

Our Competitive Strengths

We believe our strengths, described below, set us apart from our competitors and are the key drivers of our success.

Unparalleled Customer Value Proposition. Our customer value proposition is a critical driver of our business. The key components include:

| ● | Differentiated Assortment Across a Wide Variety of Hard Surface Flooring Categories. Our stores are generally larger than those of our specialty retail flooring competitors, and we allocate substantially more square footage to hard surface flooring and accessories than other large format home improvement retailers. We believe we have the most comprehensive in-stock, trend-right product assortment in the industry within our categories with on average approximately 3,800 stock keeping units (“SKUs”) in each store which, based on our market experience, is a far greater in-stock offering than any other flooring retailer. Additionally, we customize our product assortment at the store level for the regional preferences of each market. We have an ongoing product line review process across all categories that |

6