0001507079falseFY2023P3DP5DP2Yhttp://fasb.org/us-gaap/2023#AccountsPayableCurrent00015070792022-12-302023-12-2800015070792023-06-29iso4217:USD00015070792024-02-19xbrli:shares00015070792023-12-2800015070792022-12-29iso4217:USDxbrli:shares0001507079us-gaap:CommonClassAMember2023-12-280001507079us-gaap:CommonClassAMember2022-12-290001507079us-gaap:CommonClassBMember2022-12-290001507079us-gaap:CommonClassBMember2023-12-280001507079us-gaap:CommonClassCMember2023-12-280001507079us-gaap:CommonClassCMember2022-12-2900015070792021-12-312022-12-2900015070792021-01-012021-12-300001507079us-gaap:CommonClassAMemberus-gaap:CommonStockMember2020-12-310001507079us-gaap:AdditionalPaidInCapitalMember2020-12-310001507079us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-12-310001507079us-gaap:RetainedEarningsMember2020-12-3100015070792020-12-310001507079us-gaap:AdditionalPaidInCapitalMember2021-01-012021-12-300001507079us-gaap:CommonClassAMemberus-gaap:CommonStockMember2021-01-012021-12-300001507079us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-01-012021-12-300001507079us-gaap:RetainedEarningsMember2021-01-012021-12-300001507079us-gaap:CommonClassAMemberus-gaap:CommonStockMember2021-12-300001507079us-gaap:AdditionalPaidInCapitalMember2021-12-300001507079us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-12-300001507079us-gaap:RetainedEarningsMember2021-12-3000015070792021-12-300001507079us-gaap:AdditionalPaidInCapitalMember2021-12-312022-12-290001507079us-gaap:CommonClassAMemberus-gaap:CommonStockMember2021-12-312022-12-290001507079us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-12-312022-12-290001507079us-gaap:RetainedEarningsMember2021-12-312022-12-290001507079us-gaap:CommonClassAMemberus-gaap:CommonStockMember2022-12-290001507079us-gaap:AdditionalPaidInCapitalMember2022-12-290001507079us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-12-290001507079us-gaap:RetainedEarningsMember2022-12-290001507079us-gaap:AdditionalPaidInCapitalMember2022-12-302023-12-280001507079us-gaap:CommonClassAMemberus-gaap:CommonStockMember2022-12-302023-12-280001507079us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-12-302023-12-280001507079us-gaap:RetainedEarningsMember2022-12-302023-12-280001507079us-gaap:CommonClassAMemberus-gaap:CommonStockMember2023-12-280001507079us-gaap:AdditionalPaidInCapitalMember2023-12-280001507079us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-12-280001507079us-gaap:RetainedEarningsMember2023-12-28fnd:segment0001507079fnd:WarehouseFormatStoreMember2023-12-28fnd:storeutr:sqft0001507079fnd:SmallFormatStoreMember2023-12-28fnd:designStudiofnd:statefnd:distributionCenter0001507079srt:MinimumMember2022-12-302023-12-280001507079srt:MaximumMember2022-12-302023-12-280001507079fnd:FurnitureFixturesAndEquipmentMembersrt:MinimumMember2023-12-280001507079fnd:FurnitureFixturesAndEquipmentMembersrt:MaximumMember2023-12-280001507079fnd:ComputerSoftwareAndHardwareMembersrt:MinimumMember2023-12-280001507079fnd:ComputerSoftwareAndHardwareMembersrt:MaximumMember2023-12-280001507079srt:MinimumMemberus-gaap:LeaseholdImprovementsMember2023-12-280001507079srt:MaximumMemberus-gaap:LeaseholdImprovementsMember2023-12-280001507079srt:MinimumMemberfnd:BuildingsAndImprovementsMember2023-12-280001507079srt:MaximumMemberfnd:BuildingsAndImprovementsMember2023-12-280001507079us-gaap:NoncompeteAgreementsMember2023-12-280001507079us-gaap:CustomerRelationshipsMember2023-12-280001507079us-gaap:PropertyPlantAndEquipmentMember2023-12-280001507079us-gaap:PropertyPlantAndEquipmentMember2022-12-290001507079us-gaap:OtherNoncurrentLiabilitiesMember2023-12-280001507079us-gaap:OtherNoncurrentLiabilitiesMember2022-12-29xbrli:pure0001507079fnd:LaminateAndVinylMember2022-12-302023-12-280001507079fnd:LaminateAndVinylMemberus-gaap:ProductConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerProductAndServiceBenchmarkMember2022-12-302023-12-280001507079fnd:LaminateAndVinylMember2021-12-312022-12-290001507079fnd:LaminateAndVinylMemberus-gaap:ProductConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerProductAndServiceBenchmarkMember2021-12-312022-12-290001507079fnd:LaminateAndVinylMember2021-01-012021-12-300001507079fnd:LaminateAndVinylMemberus-gaap:ProductConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerProductAndServiceBenchmarkMember2021-01-012021-12-300001507079fnd:TileMember2022-12-302023-12-280001507079fnd:TileMemberus-gaap:ProductConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerProductAndServiceBenchmarkMember2022-12-302023-12-280001507079fnd:TileMember2021-12-312022-12-290001507079fnd:TileMemberus-gaap:ProductConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerProductAndServiceBenchmarkMember2021-12-312022-12-290001507079fnd:TileMember2021-01-012021-12-300001507079fnd:TileMemberus-gaap:ProductConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerProductAndServiceBenchmarkMember2021-01-012021-12-300001507079fnd:InstallationMaterialsAndToolsMember2022-12-302023-12-280001507079fnd:InstallationMaterialsAndToolsMemberus-gaap:ProductConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerProductAndServiceBenchmarkMember2022-12-302023-12-280001507079fnd:InstallationMaterialsAndToolsMember2021-12-312022-12-290001507079fnd:InstallationMaterialsAndToolsMemberus-gaap:ProductConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerProductAndServiceBenchmarkMember2021-12-312022-12-290001507079fnd:InstallationMaterialsAndToolsMember2021-01-012021-12-300001507079fnd:InstallationMaterialsAndToolsMemberus-gaap:ProductConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerProductAndServiceBenchmarkMember2021-01-012021-12-300001507079fnd:DecorativeAccessoriesAndWallTileMember2022-12-302023-12-280001507079fnd:DecorativeAccessoriesAndWallTileMemberus-gaap:ProductConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerProductAndServiceBenchmarkMember2022-12-302023-12-280001507079fnd:DecorativeAccessoriesAndWallTileMember2021-12-312022-12-290001507079fnd:DecorativeAccessoriesAndWallTileMemberus-gaap:ProductConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerProductAndServiceBenchmarkMember2021-12-312022-12-290001507079fnd:DecorativeAccessoriesAndWallTileMember2021-01-012021-12-300001507079fnd:DecorativeAccessoriesAndWallTileMemberus-gaap:ProductConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerProductAndServiceBenchmarkMember2021-01-012021-12-300001507079fnd:WoodMember2022-12-302023-12-280001507079fnd:WoodMemberus-gaap:ProductConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerProductAndServiceBenchmarkMember2022-12-302023-12-280001507079fnd:WoodMember2021-12-312022-12-290001507079fnd:WoodMemberus-gaap:ProductConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerProductAndServiceBenchmarkMember2021-12-312022-12-290001507079fnd:WoodMember2021-01-012021-12-300001507079fnd:WoodMemberus-gaap:ProductConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerProductAndServiceBenchmarkMember2021-01-012021-12-300001507079fnd:NaturalStoneMember2022-12-302023-12-280001507079fnd:NaturalStoneMemberus-gaap:ProductConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerProductAndServiceBenchmarkMember2022-12-302023-12-280001507079fnd:NaturalStoneMember2021-12-312022-12-290001507079fnd:NaturalStoneMemberus-gaap:ProductConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerProductAndServiceBenchmarkMember2021-12-312022-12-290001507079fnd:NaturalStoneMember2021-01-012021-12-300001507079fnd:NaturalStoneMemberus-gaap:ProductConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerProductAndServiceBenchmarkMember2021-01-012021-12-300001507079fnd:AdjacentCategoriesMember2022-12-302023-12-280001507079us-gaap:ProductConcentrationRiskMemberfnd:AdjacentCategoriesMemberus-gaap:RevenueFromContractWithCustomerProductAndServiceBenchmarkMember2022-12-302023-12-280001507079fnd:AdjacentCategoriesMember2021-12-312022-12-290001507079us-gaap:ProductConcentrationRiskMemberfnd:AdjacentCategoriesMemberus-gaap:RevenueFromContractWithCustomerProductAndServiceBenchmarkMember2021-12-312022-12-290001507079fnd:AdjacentCategoriesMember2021-01-012021-12-300001507079us-gaap:ProductConcentrationRiskMemberfnd:AdjacentCategoriesMemberus-gaap:RevenueFromContractWithCustomerProductAndServiceBenchmarkMember2021-01-012021-12-300001507079us-gaap:ProductAndServiceOtherMember2022-12-302023-12-280001507079us-gaap:ProductAndServiceOtherMemberus-gaap:ProductConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerProductAndServiceBenchmarkMember2022-12-302023-12-280001507079us-gaap:ProductAndServiceOtherMember2021-12-312022-12-290001507079us-gaap:ProductAndServiceOtherMemberus-gaap:ProductConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerProductAndServiceBenchmarkMember2021-12-312022-12-290001507079us-gaap:ProductAndServiceOtherMember2021-01-012021-12-300001507079us-gaap:ProductAndServiceOtherMemberus-gaap:ProductConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerProductAndServiceBenchmarkMember2021-01-012021-12-300001507079us-gaap:ProductConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerProductAndServiceBenchmarkMember2022-12-302023-12-280001507079us-gaap:ProductConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerProductAndServiceBenchmarkMember2021-12-312022-12-290001507079us-gaap:ProductConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerProductAndServiceBenchmarkMember2021-01-012021-12-300001507079us-gaap:LeaseholdImprovementsMember2023-12-280001507079us-gaap:LeaseholdImprovementsMember2022-12-290001507079fnd:BuildingsAndImprovementsMember2023-12-280001507079fnd:BuildingsAndImprovementsMember2022-12-290001507079fnd:FurnitureFixturesAndEquipmentMember2023-12-280001507079fnd:FurnitureFixturesAndEquipmentMember2022-12-290001507079fnd:ComputerSoftwareAndHardwareMember2023-12-280001507079fnd:ComputerSoftwareAndHardwareMember2022-12-290001507079us-gaap:LandMember2023-12-280001507079us-gaap:LandMember2022-12-290001507079us-gaap:ConstructionInProgressMember2023-12-280001507079us-gaap:ConstructionInProgressMember2022-12-290001507079us-gaap:CustomerRelationshipsMember2022-12-290001507079us-gaap:NoncompeteAgreementsMember2022-12-290001507079us-gaap:TradeNamesMember2023-12-280001507079us-gaap:TradeNamesMember2022-12-290001507079us-gaap:StateAndLocalJurisdictionMember2022-12-302023-12-280001507079us-gaap:StateAndLocalJurisdictionMember2021-12-312022-12-290001507079us-gaap:StateAndLocalJurisdictionMember2021-01-012021-12-300001507079us-gaap:StateAndLocalJurisdictionMember2023-12-280001507079us-gaap:FairValueInputsLevel3Member2023-12-280001507079us-gaap:FairValueInputsLevel3Memberfnd:AccruedExpensesAndOtherCurrentLiabilitiesMember2023-12-280001507079us-gaap:FairValueInputsLevel3Memberus-gaap:OtherNoncurrentLiabilitiesMember2023-12-280001507079fnd:BusinessCombinationContingentConsiderationLiabilityMember2022-12-302023-12-280001507079fnd:BusinessCombinationContingentConsiderationLiabilityMember2022-12-290001507079fnd:BusinessCombinationContingentConsiderationLiabilityMember2023-12-280001507079fnd:SalesmasterAssociatesIncMember2023-06-072023-06-070001507079fnd:SalesmasterAssociatesIncMember2023-06-070001507079us-gaap:MeasurementInputDiscountRateMember2023-12-280001507079us-gaap:MeasurementInputDiscountRateMember2022-12-290001507079us-gaap:MeasurementInputRevenueMultipleMember2023-12-280001507079us-gaap:MeasurementInputRevenueMultipleMember2022-12-290001507079us-gaap:MeasurementInputEbitdaMultipleMember2023-12-280001507079us-gaap:MeasurementInputEbitdaMultipleMember2022-12-290001507079us-gaap:InterestRateCapMemberus-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2023-12-280001507079us-gaap:InterestRateCapMemberus-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-290001507079us-gaap:InterestRateCapMemberus-gaap:AccumulatedGainLossNetCashFlowHedgeParentMember2022-12-302023-12-280001507079us-gaap:InterestRateCapMemberus-gaap:AccumulatedGainLossNetCashFlowHedgeParentMember2021-12-312022-12-290001507079fnd:TermLoanFacilityMemberfnd:InterestRateCapOneMemberus-gaap:DesignatedAsHedgingInstrumentMember2023-12-280001507079fnd:TermLoanFacilityMemberfnd:InterestRateCapOneMemberus-gaap:OtherCurrentAssetsMemberus-gaap:DesignatedAsHedgingInstrumentMember2023-12-280001507079fnd:TermLoanFacilityMemberfnd:InterestRateCapOneMemberus-gaap:OtherAssetsMemberus-gaap:DesignatedAsHedgingInstrumentMember2023-12-280001507079fnd:TermLoanFacilityMemberfnd:InterestRateCapOneMemberus-gaap:AccumulatedOtherComprehensiveIncomeMemberus-gaap:DesignatedAsHedgingInstrumentMember2023-12-280001507079fnd:TermLoanFacilityMemberus-gaap:DesignatedAsHedgingInstrumentMemberfnd:InterestRateCapTwoMember2023-12-280001507079fnd:TermLoanFacilityMemberus-gaap:OtherCurrentAssetsMemberus-gaap:DesignatedAsHedgingInstrumentMemberfnd:InterestRateCapTwoMember2023-12-280001507079fnd:TermLoanFacilityMemberus-gaap:OtherAssetsMemberus-gaap:DesignatedAsHedgingInstrumentMemberfnd:InterestRateCapTwoMember2023-12-280001507079fnd:TermLoanFacilityMemberus-gaap:AccumulatedOtherComprehensiveIncomeMemberus-gaap:DesignatedAsHedgingInstrumentMemberfnd:InterestRateCapTwoMember2023-12-280001507079fnd:TermLoanFacilityMemberfnd:InterestRateCapOneMemberus-gaap:DesignatedAsHedgingInstrumentMember2022-12-290001507079fnd:TermLoanFacilityMemberfnd:InterestRateCapOneMemberus-gaap:OtherCurrentAssetsMemberus-gaap:DesignatedAsHedgingInstrumentMember2022-12-290001507079fnd:TermLoanFacilityMemberfnd:InterestRateCapOneMemberus-gaap:OtherAssetsMemberus-gaap:DesignatedAsHedgingInstrumentMember2022-12-290001507079fnd:TermLoanFacilityMemberfnd:InterestRateCapOneMemberus-gaap:AccumulatedOtherComprehensiveIncomeMemberus-gaap:DesignatedAsHedgingInstrumentMember2022-12-290001507079fnd:TermLoanFacilityMemberus-gaap:DesignatedAsHedgingInstrumentMemberfnd:InterestRateCapTwoMember2022-12-290001507079fnd:TermLoanFacilityMemberus-gaap:OtherCurrentAssetsMemberus-gaap:DesignatedAsHedgingInstrumentMemberfnd:InterestRateCapTwoMember2022-12-290001507079fnd:TermLoanFacilityMemberus-gaap:OtherAssetsMemberus-gaap:DesignatedAsHedgingInstrumentMemberfnd:InterestRateCapTwoMember2022-12-290001507079fnd:TermLoanFacilityMemberus-gaap:AccumulatedOtherComprehensiveIncomeMemberus-gaap:DesignatedAsHedgingInstrumentMemberfnd:InterestRateCapTwoMember2022-12-290001507079us-gaap:InterestRateCapMember2022-12-302023-12-280001507079us-gaap:InterestRateCapMember2021-12-312022-12-290001507079us-gaap:InterestRateCapMember2021-01-012021-12-300001507079srt:MinimumMember2023-12-280001507079srt:MaximumMember2023-12-28fnd:lease0001507079us-gaap:SellingAndMarketingExpenseMember2022-12-302023-12-280001507079us-gaap:SellingAndMarketingExpenseMember2021-12-312022-12-290001507079us-gaap:SellingAndMarketingExpenseMember2021-01-012021-12-300001507079us-gaap:CostOfSalesMember2022-12-302023-12-280001507079us-gaap:CostOfSalesMember2021-12-312022-12-290001507079us-gaap:CostOfSalesMember2021-01-012021-12-300001507079fnd:PreOpeningCostsMember2022-12-302023-12-280001507079fnd:PreOpeningCostsMember2021-12-312022-12-290001507079fnd:PreOpeningCostsMember2021-01-012021-12-300001507079us-gaap:GeneralAndAdministrativeExpenseMember2022-12-302023-12-280001507079us-gaap:GeneralAndAdministrativeExpenseMember2021-12-312022-12-290001507079us-gaap:GeneralAndAdministrativeExpenseMember2021-01-012021-12-300001507079fnd:NguyenVInspectionsNowIncNo21DCV287142Memberus-gaap:DamagesFromProductDefectsMemberus-gaap:PendingLitigationMember2021-11-152021-11-150001507079fnd:NguyenVInspectionsNowIncNo21DCV287142Memberus-gaap:DamagesFromProductDefectsMemberus-gaap:PendingLitigationMember2022-08-082022-08-080001507079fnd:TermLoanFacilityMember2023-12-280001507079fnd:TermLoanFacilityMember2022-12-290001507079us-gaap:LineOfCreditMemberfnd:AssetBasedLoanFacilityMemberus-gaap:RevolvingCreditFacilityMember2023-12-280001507079us-gaap:LineOfCreditMemberfnd:AssetBasedLoanFacilityMemberus-gaap:RevolvingCreditFacilityMember2022-12-290001507079fnd:TermLoanFacilityMemberus-gaap:InterestRateCapMemberus-gaap:DesignatedAsHedgingInstrumentMember2023-12-280001507079us-gaap:FederalFundsEffectiveSwapRateMemberfnd:CreditAgreementMember2022-12-302023-12-280001507079us-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMemberfnd:CreditAgreementMember2022-12-302023-12-280001507079us-gaap:BaseRateMembersrt:MinimumMemberfnd:CreditAgreementMember2022-12-302023-12-280001507079us-gaap:BaseRateMembersrt:MaximumMemberfnd:CreditAgreementMember2022-12-302023-12-280001507079srt:MinimumMemberus-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMemberfnd:CreditAgreementMember2022-12-302023-12-280001507079srt:MaximumMemberus-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMemberfnd:CreditAgreementMember2022-12-302023-12-280001507079fnd:RevolvingCreditFacilityAccordionFeatureMemberus-gaap:RevolvingCreditFacilityMember2023-12-280001507079fnd:AssetBasedLoanFacilityMemberus-gaap:RevolvingCreditFacilityMember2023-12-280001507079us-gaap:LetterOfCreditMember2023-12-280001507079fnd:AssetBasedLoanFacilityMember2023-12-280001507079us-gaap:RevolvingCreditFacilityMember2023-12-280001507079us-gaap:RevolvingCreditFacilityMember2022-12-290001507079fnd:TermLoanFacilityMemberus-gaap:FairValueInputsLevel3Member2023-12-280001507079fnd:TermLoanFacilityMemberus-gaap:FairValueInputsLevel3Member2022-12-290001507079us-gaap:LineOfCreditMemberfnd:AssetBasedLoanFacilityMemberus-gaap:RevolvingCreditFacilityMemberus-gaap:FairValueInputsLevel2Member2023-12-280001507079us-gaap:LineOfCreditMemberfnd:AssetBasedLoanFacilityMemberus-gaap:RevolvingCreditFacilityMemberus-gaap:FairValueInputsLevel2Member2022-12-29fnd:classfnd:vote0001507079fnd:StockOptionPlan2011Member2016-12-290001507079fnd:StockOptionPlan2011Member2015-12-310001507079fnd:StockIncentivePlan2017Member2017-04-130001507079fnd:StockIncentivePlan2017Member2023-05-100001507079fnd:StockIncentivePlan2017Member2023-12-280001507079fnd:StockIncentivePlan2017Member2022-12-290001507079us-gaap:EmployeeStockOptionMember2022-12-302023-12-280001507079srt:MinimumMemberus-gaap:EmployeeStockOptionMember2022-12-302023-12-280001507079srt:MaximumMemberus-gaap:EmployeeStockOptionMember2022-12-302023-12-280001507079us-gaap:EmployeeStockOptionMember2021-12-312022-12-290001507079us-gaap:EmployeeStockOptionMember2021-01-012021-12-300001507079us-gaap:EmployeeStockOptionMember2023-12-280001507079us-gaap:EmployeeStockOptionMember2022-12-290001507079fnd:PerformanceBasedRestrictedStockUnitsMember2022-12-302023-12-280001507079srt:MinimumMembersrt:ExecutiveOfficerMemberfnd:OneTimeShareBasedCompensationGrantMemberfnd:PerformanceBasedRestrictedStockUnitsMember2022-12-302023-12-280001507079srt:MaximumMembersrt:ExecutiveOfficerMemberfnd:OneTimeShareBasedCompensationGrantMemberfnd:PerformanceBasedRestrictedStockUnitsMember2022-12-302023-12-280001507079srt:MinimumMemberfnd:PerformanceBasedRestrictedStockUnitsMemberfnd:AnnualShareBasedCompensationGrantMember2022-12-302023-12-280001507079srt:MaximumMemberfnd:PerformanceBasedRestrictedStockUnitsMemberfnd:AnnualShareBasedCompensationGrantMember2022-12-302023-12-280001507079srt:MinimumMemberfnd:TotalShareholderReturnUnitsMembersrt:ExecutiveOfficerMemberfnd:OneTimeShareBasedCompensationGrantMember2022-12-302023-12-280001507079srt:MaximumMemberfnd:TotalShareholderReturnUnitsMembersrt:ExecutiveOfficerMemberfnd:OneTimeShareBasedCompensationGrantMember2022-12-302023-12-280001507079fnd:TotalShareholderReturnUnitsMember2022-12-302023-12-280001507079srt:MinimumMemberus-gaap:RestrictedStockUnitsRSUMember2022-12-302023-12-280001507079srt:MaximumMemberus-gaap:RestrictedStockUnitsRSUMember2022-12-302023-12-280001507079fnd:ServiceBasedRestrictedStockUnitsMember2022-12-290001507079fnd:PerformanceBasedRestrictedStockUnitsMember2022-12-290001507079fnd:TotalShareholderReturnUnitsMember2022-12-290001507079fnd:ServiceBasedRestrictedStockUnitsMember2022-12-302023-12-280001507079fnd:ServiceBasedRestrictedStockUnitsMember2023-12-280001507079fnd:PerformanceBasedRestrictedStockUnitsMember2023-12-280001507079fnd:TotalShareholderReturnUnitsMember2023-12-280001507079us-gaap:RestrictedStockUnitsRSUMember2023-12-280001507079us-gaap:RestrictedStockUnitsRSUMember2022-12-290001507079us-gaap:RestrictedStockUnitsRSUMember2022-12-302023-12-280001507079us-gaap:RestrictedStockUnitsRSUMember2021-12-312022-12-290001507079us-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-300001507079fnd:ServiceBasedShareAwardsMember2022-12-290001507079fnd:PerformanceBasedShareAwardsMember2022-12-290001507079fnd:TotalShareholderReturnAwardsMember2022-12-290001507079fnd:ServiceBasedShareAwardsMember2022-12-302023-12-280001507079fnd:PerformanceBasedShareAwardsMember2022-12-302023-12-280001507079fnd:TotalShareholderReturnAwardsMember2022-12-302023-12-280001507079fnd:ServiceBasedShareAwardsMember2023-12-280001507079fnd:PerformanceBasedShareAwardsMember2023-12-280001507079fnd:TotalShareholderReturnAwardsMember2023-12-280001507079fnd:PerformanceBasedAndTotalShareholderReturnRestrictedStockAwardsMember2022-12-302023-12-280001507079fnd:RestrictedStockAwardMember2023-12-280001507079fnd:RestrictedStockAwardMember2022-12-290001507079fnd:RestrictedStockAwardMember2022-12-302023-12-280001507079fnd:RestrictedStockAwardMember2021-12-312022-12-290001507079fnd:RestrictedStockAwardMember2021-01-012021-12-300001507079us-gaap:CommonClassAMemberfnd:EmployeeStockPurchasePlanMember2023-12-280001507079fnd:EmployeeStockPurchasePlanMember2022-12-302023-12-280001507079fnd:EmployeeStockPurchasePlanMember2021-12-312022-12-290001507079fnd:EmployeeStockPurchasePlanMember2021-01-012021-12-300001507079us-gaap:EmployeeStockOptionMember2022-12-302023-12-280001507079us-gaap:EmployeeStockOptionMember2021-12-312022-12-290001507079us-gaap:EmployeeStockOptionMember2021-01-012021-12-300001507079us-gaap:RestrictedStockUnitsRSUMember2022-12-302023-12-280001507079us-gaap:RestrictedStockUnitsRSUMember2021-12-312022-12-290001507079us-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-3000015070792022-12-302023-03-3000015070792023-03-312023-06-2900015070792023-06-302023-09-2800015070792023-09-292023-12-2800015070792021-12-312022-03-3100015070792022-04-012022-06-3000015070792022-07-012022-09-2900015070792022-09-302022-12-290001507079fnd:SalesmasterAssociatesIncMember2022-12-302023-12-280001507079fnd:SpartanSurfacesIncMember2021-01-012021-12-300001507079fnd:SalesmasterAssociatesIncMemberus-gaap:CustomerRelationshipsMember2023-06-070001507079fnd:SalesmasterAssociatesIncMemberus-gaap:CustomerRelationshipsMember2023-06-072023-06-070001507079fnd:SpartanSurfacesIncMember2021-06-040001507079fnd:SpartanSurfacesIncMember2021-06-042021-06-040001507079fnd:SpartanSurfacesIncMemberfnd:AnnualEarningsMarginTargetsMember2021-06-040001507079fnd:AnnualGrossProfitTargetsMemberfnd:SpartanSurfacesIncMember2021-06-040001507079fnd:CommercialFlooringSalesDistributorsAcquisitionMember2021-12-312022-12-29fnd:distributor0001507079fnd:CommercialFlooringSalesDistributorsAcquisitionMember2022-12-290001507079fnd:CommercialFlooringSalesDistributorsAcquisitionMemberus-gaap:CustomerRelationshipsMember2022-12-290001507079fnd:CommercialFlooringSalesDistributorsAcquisitionMemberus-gaap:CustomerRelationshipsMember2021-12-312022-12-290001507079fnd:TermLoanFacilityMemberus-gaap:InterestRateCapMemberus-gaap:DesignatedAsHedgingInstrumentMemberus-gaap:SubsequentEventMember2024-01-150001507079fnd:TermLoanFacilityMemberus-gaap:InterestRateCapMemberus-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMemberus-gaap:DesignatedAsHedgingInstrumentMemberus-gaap:SubsequentEventMember2024-01-15

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| | | | | |

☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 28, 2023

OR

| | | | | |

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ____ to ____

Commission file number 001-38070

Floor & Decor Holdings, Inc.

(Exact name of registrant as specified in its charter)

| | | | | | | | |

| Delaware | | 27-3730271 |

(State or Other Jurisdiction of Incorporation or Organization) | | (I.R.S. Employer Identification No.) |

| | | | | | | | | | | | | | |

| 2500 Windy Ridge Parkway SE | | |

| Atlanta, | Georgia | | 30339 |

| (Address of principal executive offices) | | (Zip Code) |

Registrant’s telephone number, including area code (404) 471-1634

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Class A Common Stock, $0.001 par value per share | FND | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | |

| Large accelerated filer | ☒ | Accelerated filer | ☐ |

| Non-accelerated filer | ☐ | Smaller reporting company | ☐ |

| | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing

reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by

any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the Registrant’s Common Stock held by non-affiliates as of June 29, 2023, based on the closing sale price per share as reported by the New York Stock Exchange on such date, was $10.8 billion. There were 106,766,587 shares of Common Stock outstanding as of February 19, 2024.

Documents Incorporated by Reference:

Portions of the Registrant’s proxy statement for the Annual Meeting of Shareholders to be filed pursuant to Regulation 14A of the Exchange Act on or before April 26, 2024, are incorporated by reference into Part III of this Form 10-K. Except as expressly incorporated by reference, the Registrant’s proxy statement shall not be deemed to be part of this report.

TABLE OF CONTENTS

| | | | | | | | |

| |

|

| | |

| Item 1 | | |

| Item 1A | | |

| Item 1B | | |

Item 1C | | |

| Item 2 | | |

| Item 3 | | |

| Item 4 | | |

| | |

|

| | |

| Item 5 | | |

| Item 6 | | |

| Item 7 | | |

| Item 7A | | |

| Item 8 | | |

| Item 9 | | |

| Item 9A | | |

| Item 9B | | |

| Item 9C | | |

| | |

|

| | |

| Item 10 | | |

| Item 11 | | |

| Item 12 | | |

| Item 13 | | |

| Item 14 | | |

| | |

|

| | |

| Item 15 | | |

| Item 16 | | |

| | |

FORWARD-LOOKING STATEMENTS.

The discussion in this Annual Report on Form 10-K (this “Annual Report”), including under Item 1A, “Risk Factors” and 1C, “Cybersecurity” of Part I and Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” of Part II, contains forward-looking statements within the meaning of the federal securities laws. All statements other than statements of historical fact contained in this Annual Report, including statements regarding our future operating results and financial position, business strategy and plans, and objectives of management for future operations, are forward-looking statements. These statements are based on our current expectations, assumptions, estimates and projections. These statements involve known and unknown risks, uncertainties, and other important factors that may cause our actual results, performance or achievements to be materially different from any future results, performance, or achievements expressed or implied by the forward-looking statements. Forward-looking statements are based on management’s current expectations and assumptions regarding the Company’s business, the economy, and other future conditions, including the impact of natural disasters on sales. In some cases, you can identify forward-looking statements by terms such as “may,” “will,” “should,” “expects,” “plans,” “anticipates,” “could,” “seeks,” “intends,” “target,” “projects,” “contemplates,” “believes,” “estimates,” “predicts,” “budget,” “potential,” or “continue” or the negative of these terms or other similar expressions.

The forward-looking statements contained in this Annual Report are only predictions. Although we believe that the expectations reflected in the forward-looking statements in this Annual Report are reasonable, we cannot guarantee future events, results, performance, or achievements. A number of important factors could cause actual results to differ materially from those indicated by the forward-looking statements in this Annual Report, including, without limitation, those factors described in Item 1A, “Risk Factors” of Part I of this Annual Report, Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” of Part II of this Annual Report, and elsewhere in the Company’s filings with the Securities and Exchange Commission (the “SEC”). Some of the key factors that could cause actual results to differ from our expectations include the following:

•an overall decline in the health of the economy, the hard surface flooring industry, consumer confidence and discretionary spending, and the housing market, including as a result of rising inflation or interest rates;

•our failure to successfully manage the challenges that our planned new store growth poses or the impact of unexpected difficulties or higher costs during our expansion;

•our inability to enter into leases for additional stores on acceptable terms or renew or replace our current store leases;

•our failure to successfully anticipate and manage trends, consumer preferences, and demand;

•our inability to successfully manage increased competition;

•our inability to manage our inventory, including the impact of inventory obsolescence, shrinkage, and damage;

•any disruption in our distribution capabilities, supply chain, and our related planning and control processes, including carrier capacity constraints, port congestion, transportation costs, and other supply chain costs or product shortages;

•any increases in wholesale prices of products, materials, and transportation costs beyond our control, including increases in costs due to inflation;

•the resignation, incapacitation, or death of any key personnel, including our executive officers;

•our inability to attract, hire, train, and retain highly qualified managers and staff;

•the impact of any labor activities;

•our dependence on foreign imports for the products we sell, including risks associated with obtaining products from abroad;

•geopolitical risks, such as the conflict in the Middle East, the ongoing war in Ukraine, and U.S. policies related to global trade and tariffs, such as import restrictions under the Uyghur Forced Labor Prevention Act, which impact our ability to import from foreign suppliers or raise our costs;

•our ability to manage our comparable store sales growth;

•any failure by any of our suppliers to supply us with quality products on attractive terms and prices;

•any failure by our suppliers to adhere to the quality standards that we set for our products;

•our inability to locate sufficient suitable natural products, particularly products made of more exotic species or unique stone;

•the effects of weather conditions, natural disasters, or other unexpected events, including public health crises that may disrupt our operations;

•our inability to maintain sufficient levels of cash flow or liquidity to fund our expanding business and service our existing indebtedness;

•any allegations, investigations, lawsuits, or violations of laws and regulations applicable to us, our products or our suppliers;

•our inability to adequately protect the privacy and security of information related to our customers, us, our associates, our suppliers, and other third parties;

•any material disruption in our information systems, including our website;

•new or changing laws or regulations, including tax laws and trade policies and regulations;

•any failure to protect our intellectual property rights or disputes regarding our intellectual property or the intellectual property of third parties;

•the impact of any future strategic transactions;

•restrictions imposed by our indebtedness on our current and future operations, including risks related to our variable rate debt; and

•our ability to manage risks related to corporate social responsibility.

Because forward-looking statements are inherently subject to risks and uncertainties, some of which cannot be predicted or quantified, you should not rely on these forward-looking statements as predictions of future events. The forward-looking statements contained in this Annual Report speak only as of the date hereof. New risks and uncertainties arise over time, and it is not possible for us to predict those events or how they may affect us. If a change to the events and circumstances reflected in our forward-looking statements occurs, our business, financial condition, and operating results may vary materially from those expressed in our forward-looking statements. Except as required by applicable law, we do not plan to publicly update or revise any forward-looking statements contained herein, whether as a result of any new information, future events, or otherwise.

PART I

ITEM 1. BUSINESS.

Except where the context suggests otherwise, the terms “Floor & Decor Holdings, Inc.,” “Floor & Decor,” the “Company,” “we,” “us,” and “our” refer to Floor & Decor Holdings, Inc., a Delaware corporation, together with its consolidated subsidiaries.

Our fiscal year is the 52- or 53-week period ending on the Thursday on or preceding December 31. The following discussion contains references to fiscal 2019, fiscal 2020, fiscal 2021, fiscal 2022, fiscal 2023, and fiscal 2024, which represent our fiscal years ended or ending, as applicable, December 26, 2019, December 31, 2020, December 30, 2021, December 29, 2022, December 28, 2023, and December 26, 2024. Fiscal years 2019, 2021, 2022, 2023, and 2024 are 52-week periods, and fiscal 2020 is a 53-week period.

Our Company

Founded in 2000, Floor & Decor is a high-growth, differentiated, multi-channel specialty retailer of hard surface flooring and related accessories and seller of commercial surfaces. Floor & Decor Holdings, Inc. was incorporated as a Delaware corporation in October 2010 in connection with the acquisition of Floor and Decor Outlets of America, Inc. in November 2010 by our previous sponsor owners. As of December 28, 2023, we operated 221 warehouse-format stores and five small design studios across 36 states. We believe that we offer the industry’s broadest in-stock assortment of tile, wood, laminate and vinyl, and natural stone flooring along with decorative and installation accessories and adjacent categories at everyday low prices positioning us as the one-stop destination for our customers’ entire hard surface flooring needs. We appeal to a variety of customers, including professional installers and commercial businesses (“Pro”) and homeowners, which are comprised of do it yourself customers (“DIY”) and buy it yourself customers who buy the products for professional installation (“BIY”).

Our warehouse-format stores, which average approximately 78,000 square feet, are typically larger than any of our specialty retail flooring competitors’ stores. Other large format home improvement retailers only allocate a small percentage of their floor space to hard surface flooring and accessories. By carrying a deep level of in-stock hard surface flooring inventory and wide range of tools and accessories, we seek to offer our customers immediate availability of everything they need to complete their entire flooring or remodeling project. In addition to our stores, our website FloorandDecor.com showcases our products, offers informational training and design ideas and has our products available for sale, which a customer can pick up in-store or have delivered. Our ability to purchase directly from manufacturers through our direct sourcing model enables us to be fast to market with a balanced assortment of best-seller and unique, hard-to-find items that are the latest trend-right products. We believe these factors create a differentiated value proposition for Floor & Decor and drive customer loyalty with our Pro and homeowner customers in our markets.

Our Competitive Strengths

We believe our strengths, described below, set us apart from our competitors and are the key drivers of our success.

Unparalleled Customer Value Proposition. Our customer value proposition is a critical driver of our business. The key components include:

•Differentiated Assortment Across a Wide Variety of Hard Surface Flooring Categories. We carry a comprehensive in-stock, trend-right product assortment with on average approximately 4,500 stock keeping units (“SKUs”) in each store which, based on our market experience, is a far greater in-stock offering than any other flooring retailer. Additionally, we customize our product assortment at the store level for the local preferences of each market. We work with our suppliers to quickly introduce new products and styles in our stores. We appeal to a wide range of customers through our “good/better/best” merchandise selection, our broad range of product styles from classic to modern, and our new trend-right products. We consistently innovate with proprietary brands.

•Low Prices. We leverage our ability to source directly from manufacturers and quarries to offer our flooring products and related accessories at everyday low prices throughout the year instead of engaging in frequent promotional activities. We believe this strategy creates trust with our customers because they consistently receive low prices at Floor & Decor without having to wait for a sale or negotiate to obtain the lowest price.

•One-Stop Project Destination with Immediate Availability. We carry an extensive range of products, including flooring and decorative accessories, as well as installation materials and tools, to fulfill a customer’s entire flooring project. In addition, we have adjacent categories such as vanities, bathroom accessories, shower doors, and custom countertops. Our stores carry a large in-stock assortment and job size quantities to differentiate us from our competitors. When a product is not available in the store, our four regional distribution centers and neighboring stores can often quickly ship the product to meet a customer’s needs. Customers also have access to our full catalog of inventory for in-store pick up or delivery through FloorandDecor.com.

Unique and Inspiring Shopping Environment. Our stores are typically designed with warehouse features including high ceilings, clear signage, bright lighting, and industrial racking and are staffed with knowledgeable store associates. We offer an easy-to-navigate store layout with clear lines of sight and departments organized by our major product categories and we invest heavily in large, visually inspiring merchandise displays that showcase our assortment as well as marketing throughout our stores to highlight product features, benefits, and design elements. These features educate and enable customers to visualize how the product would look in their homes or businesses. The majority of our stores have design centers, with multiple different vignettes that showcase project ideas to further inspire our customers, and we employ experienced designers in all of our stores to provide free design consulting. Additionally, we provide a robust online experience for potential customers on FloorandDecor.com.

Extensive Service Offerings to Enhance the Pro Customer Experience. We provide an efficient one-stop shopping experience for our Pro customers, offering low prices on a broad selection of high-quality flooring products, deep inventory levels to support immediate availability of our products, credit offerings, free storage for purchased inventory, the convenience of early store hours, and separate entrances for merchandise pick-up. We also offer Design Services, which helps our Pro customers serve their customers. Additionally, each store has a dedicated Pro sales force with technology to service our Pro customer more efficiently. We have a Pro loyalty rewards program, which provides awards points based on purchases and business-building tools. Rewarding our Pro customers through this program improves their loyalty to Floor & Decor, and by serving the needs of Pro customers, we drive repeat and high-ticket purchases, customer referrals, and brand awareness from this attractive and loyal customer segment.

Decentralized Culture with an Experienced Store-Level Team and Emphasis on Training. We have a decentralized culture that empowers managers at the store and regional levels to make key decisions to maximize the customer experience. Our store managers, who carry the title Chief Executive Merchant (“CEM”), have significant flexibility to customize product mix, pricing, marketing, merchandising, visual displays and other elements in consultation with their regional leaders. We create or implement localized assortments, which are not only trend-forward but often create trends in the industry, which we believe differentiates us from our national competitors, which tend to have standard assortments across markets. Throughout the year, we regularly train all of our employees on a variety of topics, including product knowledge, sales strategies, leadership and store operations. Our store managers and store department managers are an integral part of our company, and many have years of relevant industry experience in retail.

Sophisticated, Global Supply Chain. Our merchandising team has developed direct sourcing relationships with manufacturers and quarries in 26 countries. We currently source our products from more than 240 vendors worldwide and have developed long-term relationships with many of them. We often collaborate with our vendors to design products for us to address emerging customer preferences that we observe in our stores and markets. We procure the majority of our products directly from manufacturers, which eliminates additional costs from exporters, importers, wholesalers, and distributors. Direct sourcing is a key competitive advantage, as many of our specialty retail flooring competitors are too small to have the scale or the resources to work directly with suppliers.

Highly Experienced Management Team with a Proven Track Record. Led by our Chief Executive Officer, Tom Taylor, our management team brings substantial expertise from leading retailers and other companies across various core functions, including store operations, merchandising, marketing, real estate, e-commerce, supply chain management, finance, legal, and information technology. Tom Taylor, who joined us in 2012, spent 23 years at The Home Depot, where he helped expand the store base from fewer than 15 stores to over 2,000 stores. Our President, Trevor Lang, was promoted to President in November 2022 after serving as the Executive Vice President and Chief Financial Officer since 2014 and Chief Financial Officer since 2011. He brings more than 25 years of executive leadership experience. In November 2022, Bryan Langley was promoted to serve as Executive Vice President and Chief Financial Officer. He joined the Company in 2014, and has served in various positions of increasing responsibility in corporate strategy, financial planning, and accounting. Our entire management team drives our organization with a focus on strong merchandising, superior customer experience, expanding our store footprint, and fostering a strong, decentralized culture.

Our Growth Strategy

We expect to drive growth in net sales and profitability through the following strategies:

Open Warehouse-Format Stores in New and Existing Markets. Based on our internal research with respect to housing density, demographic data, competitor concentration and other variables in both new and existing markets, we believe there is an opportunity to significantly expand our warehouse-format store base by a low- to mid-teens annual percentage growth rate over the near-to-medium term, reaching at least 500 in the United States within approximately eight years. We plan to target new store openings in both new and existing, adjacent, and underserved markets. We have a disciplined approach to new store development based on an analytical, research-driven site selection method and a rigorous real estate approval process. Our new store model targets on average net sales of $14 million to $16 million and four-wall adjusted EBITDA before pre-opening expenses of $2.5 million to $3.5 million during the first full year of operation, pre-tax payback in approximately two and a half to three and a half years and cash-on-cash returns of approximately 50% in the third year. Based on challenging macroeconomic conditions, our class of 2022 and class of 2023 new stores are estimated to be below these targets. Our historical new store performance, the performance of our more mature stores, our disciplined real estate strategy, and the track record of our management team in successfully opening retail stores support our belief in the significant store expansion opportunity.

Increase Comparable Store Sales. We expect to grow comparable store sales over the long-term by continuing to offer our customers a dynamic and expanding selection of compelling, value-priced hard surface flooring and accessories while maintaining strong service standards. Because approximately 55% of our stores have been open for less than five years, we believe they will continue to drive comparable store sales growth as newer stores ramp up to maturity. We believe that we can continue to enhance our customer experience by focusing on service, optimizing sales and marketing strategies, investing in store staff and infrastructure, remodeling existing stores, and improving visual merchandising and the overall aesthetic appeal of our stores. We also believe that growing our proprietary credit offering, Pro, Commercial, and design strategies, further integrating connected customer strategies, and enhancing other key information technology, will contribute to increased comparable store sales. As we increase awareness of Floor & Decor’s brand, we believe there is a significant opportunity to gain additional market share.

Expand Our “Connected Customer” Experience. Floor & Decor’s online experience allows our customers to explore our product selection and design ideas before and after visiting our stores and offers the convenience of making online purchases for delivery or pick up in-store. We believe our online platform reflects our brand attributes and provides a powerful tool to educate, inspire, and engage our consumers. We continuously invest in our connected customer strategies to improve how customers experience our brand. For example, we regularly enhance our website, which provides our customers with inspirational vignettes, videos, products, a room visualizer, education, and a faster online shopping experience. Our connected customer sales represented approximately 19% of our total net sales for fiscal 2023. While the hard surface flooring category has a relatively low penetration of connected customer sales due to the nature of the product, we believe our connected customer presence represents an attractive growth opportunity to drive consumers to Floor & Decor.

Continue to Invest in the Pro Customer. We believe our differentiated focus on Pro customers has created a competitive advantage for us and will continue to drive net sales growth. We continue to invest in gaining and retaining Pro customers due to their frequent and high-ticket purchases, loyalty, and propensity to refer other potential customers. We have made important investments in the Pro services regional team to better recruit and train the Pro services team in each store. We have also invested in technology to help us further penetrate and grow our Pro business. We continue to invest in refreshing and expanding our services to Pros to better facilitate our growing Pro business.

Continue to Invest in Design Services. Our Design Services offer a unique experience to large format retail, which leads our customers through a seamless, inspirational design process to complete their projects. According to our internal research, when a designer is involved, customer satisfaction and average ticket is higher, and customers are more likely to follow through with a purchase. We invest in recruiting top design talent and provide extensive design-focused training, tools, and technology to ensure our teams are knowledgeable and prepared to deliver a start-to-finish consultative selling experience.

Expand Our Sales Growth in Commercial Surfaces. We continue to grow our commercial surfaces business both organically and through acquisitions, applying many of the same strategies that have allowed us to be successful in selling residential retail hard surface flooring, including high quality, trend-right hard surface flooring sourced at a low cost directly from the manufacturer. We intend to continue to focus on both organic and inorganic growth to address the entire commercial surfaces market.

Enhance Margins Through Increased Operating Leverage. Operating margin improvement opportunities will include enhanced product sourcing processes and overall leveraging of our store-level fixed costs, existing infrastructure, supply chain, corporate overhead and other fixed costs resulting from increased sales productivity. We anticipate that the planned expansion of our store base and growth in comparable store sales will also support increasing economies of scale over the long-term while still making significant investments in our business.

Our Industry

Floor & Decor operates in the large, growing, and highly fragmented U.S. retail hard surface flooring market and commercial surfaces market. We believe that growth in the hard surface flooring market will continue to be driven by several home remodeling demand drivers. These include a large supply of aging homes, millennials entering their household formation years, existing-home sales growth from the low supply of housing inventory, rising home equity values, and the secular shift from carpet to hard surface flooring. In addition, we believe we have an opportunity to increase our market share as many of our competitors are unable to effectively compete with our combination of price, service, and broad in-stock assortment. The competitive landscape of the hard surface flooring market includes big-box home improvement centers, national and regional specialty flooring retailers, independent flooring retailers, and distributors.

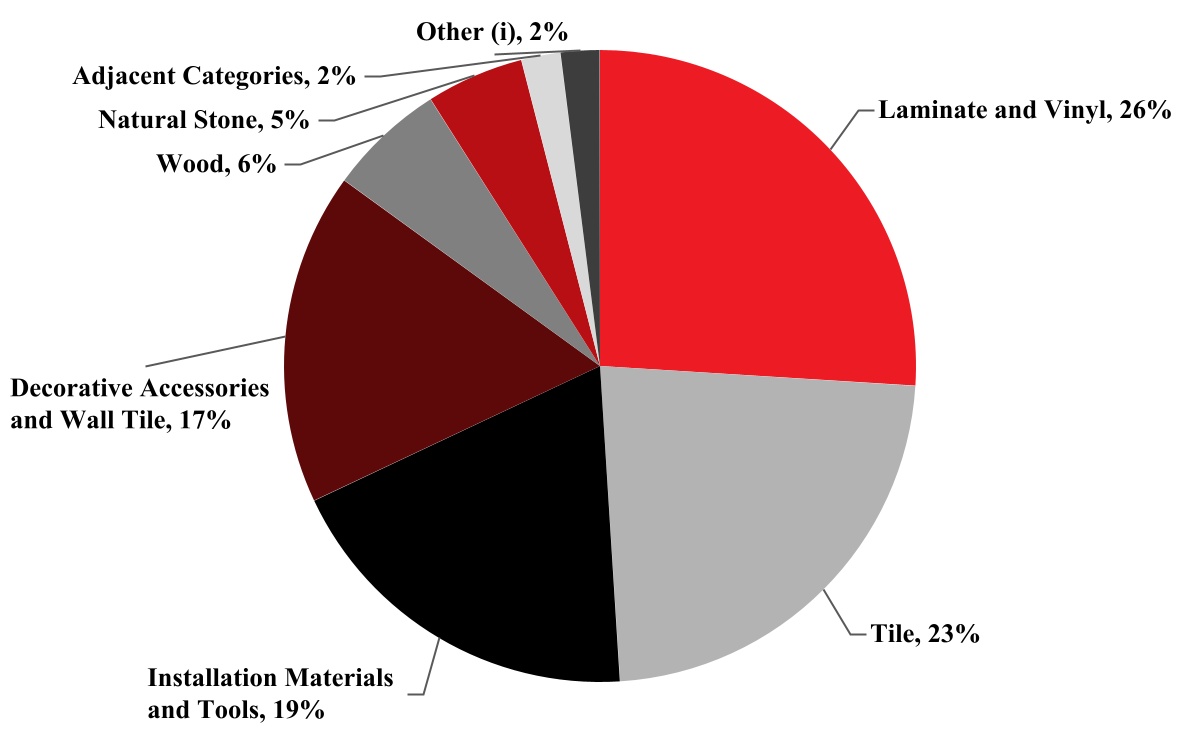

We believe we have an opportunity to continue to gain share in the hard surface flooring market with the largest in-stock selection of laminate and vinyl, tile, installation materials, decorative accessories, wood, and natural stone. Our strong focus on the customer experience drives us to remain innovative and locally relevant while maintaining low prices and in-stock merchandise in a one-stop shopping destination.

Our Products

Our merchandise is comprised of the following major product categories:

•Laminate and vinyl: Wood-based laminate flooring, luxury vinyl, and engineered/composite (rigid core) vinyl.

•Tile: Porcelain and ceramic.

•Installation materials and tools: Grout, mortar, backer board, tools, adhesives, underlayments, moldings, and stair treads.

•Decorative accessories and wall tile: Glass, natural stone, tile mosaics, decorative tiles, decorative trims, and wall tile.

•Wood: Solid prefinished hardwood, solid unfinished hardwood, engineered hardwood, bamboo, and wood countertops.

•Natural stone: Marble, limestone, travertine, slate, ledger, prefabricated countertops, thresholds, and shower benches.

•Adjacent categories: Vanities, shower doors, bath accessories, faucets, sinks, custom countertops, bathroom mirrors, and bathroom lighting.

Our fiscal 2023 net sales by major product category are set forth below:

(i) Other includes delivery, sample, and other product revenue and adjustments for deferred revenue, sales returns reserves, and other revenue related adjustments that are not allocated on a product-level basis. Refer to Note 2, “Revenue” of the notes to our consolidated financial statements included in this Annual Report for more information.

Store Development

Most of our stores are situated in highly visible retail and industrial locations. We have developed a disciplined approach to new store development, based on an analytical, research-driven method to site selection and a rigorous real estate review and approval process. By focusing on key demographic characteristics for new site selection, such as aging of homes, length of home ownership and median income, we expect to open new stores with attractive returns. When opening new stores, inventory orders are placed several months prior to a new store opening. Significant investment is made in building out or constructing the site, hiring and training employees in advance, and marketing the new store through pre-opening events to draw the flooring industry community together. Each new store is thoughtfully designed with store interiors that include vignettes and interchangeable displays, racking to access products to allow ease of shopping, and an exterior highlighted by a large, bold Floor & Decor sign.

Connected Customer

We aim to elevate the total customer experience through our website FloorandDecor.com. Enhancements to our connected customer experience are critical to our increasingly interconnected customers who often perform extensive online research for their project before going to our store. FloorandDecor.com is an important tool for engaging our homeowner customers throughout their process. Our Pro customers use the website and our Pro app to browse our broad product assortment, to continually educate themselves on new techniques and trends and to share our virtual catalog and design ideas with their customers and utilize tools such as our calculators to aid with shopping. We designed the website to be a reflection of our stores and to promote our wide selection of high quality products and low prices. To this end, we believe the website provides not only the same region-specific product selection that customers can expect in our stores, but also the opportunity to extend our assortment by offering our entire portfolio of products.

In addition to highlighting our broad product selection, FloorandDecor.com offers a convenient opportunity for customers to purchase products online and pick them up in our stores. As we continue to grow, we believe connected customer will become an increasingly important part of our strategy.

Marketing and Advertising

We use a multi-platform approach to increasing Floor & Decor’s brand awareness, while historically maintaining low advertising costs as a percentage of net sales of approximately 3%. We use traditional advertising media, combined with social media and online marketing, to share the Floor & Decor story with a growing audience. We take the same customized approach with our marketing as we do with our product selection; each region has a varied media mix based on local trends and what we believe will most efficiently drive sales. To further enhance our targeting efforts, our store managers have input into their respective stores’ marketing spend.

Sourcing

Floor & Decor has a well-developed and geographically diverse supplier base. Our largest supplier accounted for 13% of our net sales in fiscal 2023, while no other individual supplier accounted for more than 10% of our net sales. We are focused on bypassing importers, exporters, wholesalers, distributors, and other middlemen in our supply chain in order to reduce costs and lead time. Our direct sourcing model and the resulting relationships we have developed with our suppliers are distinct competitive advantages. The cost savings we achieve by directly sourcing our merchandise enable us to offer our customers low prices.

We have established a Global Sourcing and Compliance Department to, among other things, enhance our policies and procedures with respect to addressing compliance with appropriate regulatory bodies, including compliance with the requirements of the Lacey Act of 1900, the California Air Resources Board, and the Environmental Protection Agency. This department also addresses compliance with Floor & Decor’s supplier compliance policies, such as specifications and packaging of the products we purchase. We utilize third-party consultants for audits, testing, and surveillance to ensure product safety and compliance. We have invested in technology and personnel to collaborate throughout the entire supply chain process. Additionally, our close relationships with suppliers allow us to collaborate with them directly to develop and quickly introduce innovative and quality products that meet our customers’ evolving tastes and preferences at low prices.

Distribution and Order Fulfillment

Merchandise inventory is our most significant working capital asset and is considered “in-transit” or “available for sale”, based on whether we have physically received the products at an individual store location or in one of our four distribution centers. In-transit inventory generally varies due to contractual terms, country of origin, transit times, international holidays, weather patterns and other factors.

We have invested significant resources to develop and enhance our distribution network. We have four distribution centers strategically located across the United States in port cities near Savannah, Houston, Los Angeles, and Baltimore and a transload facility near Los Angeles. Third-party brokers arrange the shipping of our international and domestic purchases to our distribution centers and stores and bill us for shipping costs according to the terms of the purchase agreements with our suppliers. All of our distribution centers are Company-operated facilities, and we have implemented a warehouse management and transportation management system tailored to our unique needs across all distribution centers. We believe this system helps service levels, reduces shrinkage and damage, helps us better manage our inventory, and allows us to better implement our connected customer initiatives. We plan to continue to seek further opportunities to enhance our distribution capabilities and align them with our strategic growth initiatives.

Management Information Systems

Technology plays a crucial role in the continued growth and success of our business. We have sought to integrate technology into all facets of our business, including supply chain, merchandising, store operations, point-of-sale, e-commerce, finance, accounting, and human resources. The integration of technology allows us to analyze the business in real time and react accordingly. Our inventory management system is our primary tool for forecasting and placing orders and managing in-stock inventory. The data-driven platform includes sophisticated forecasting tools based on historical trends in sales, inventory levels and vendor lead times at the store and distribution center level by SKU, allowing us to support store managers in their regional merchandising efforts. We rely on the forecasting accuracy of our system to maintain the in-stock, job-lot quantities that our customers rely on.

Competition

The retail hard surface flooring market is highly fragmented and competitive. We face significant competition from large home improvement centers, national and regional specialty flooring chains, and independent flooring retailers. Some of our competitors are organizations that are larger, better capitalized, have existed longer, have product offerings that extend beyond hard surface flooring and related accessories, and have a more established market presence with substantially greater resources than we have. In addition, while the hard surface flooring category has a relatively low threat of new internet-only entrants due to the nature of the product, the growth opportunities presented by e-commerce could outweigh these challenges and result in increased competition in this portion of our connected customer strategy. Further, because the barriers to entry into the hard surface flooring industry are relatively low, manufacturers and suppliers of flooring and related products, including those whose products we currently sell, could enter the market and start directly competing with us.

We believe the key competitive factors in the retail hard surface flooring industry include localized product assortment, product innovation, in-store availability of products in job-lot quantities, product sourcing, product presentation, customer service, store management, store location, and low prices. We believe that we compete favorably with respect to each of these factors by providing a highly diverse selection of products to our customers, at an attractive value, in appealing and convenient retail stores.

Human Capital

We have built a strong team of employees to support our continued success. Each of our stores is led by a CEM and is supported by an operations manager, product category department managers, a design team, a Pro sales and support team, and a number of additional associates. Outside of our stores, we have employees dedicated to corporate, store support, infrastructure, e-commerce, call center and similar functions as well as support for our distribution centers and sourcing office. We dedicate significant resources to training our employees as they are key to our success. Our Chief Human Resources Officer, supported by the entire executive team, is responsible for developing and executing our human capital strategy. This includes the attraction, development, engagement, safety, and retention of talent and the design of associate compensation and benefits programs.

As of December 28, 2023, we had 12,783 employees, 9,857 of whom were full-time. Of the total employees, 10,889 work in our stores, 1,423 work in corporate, store support, customer care or similar functions, 459 work in distribution centers, and 12 work in our Asia sourcing office in Shanghai, China.

Currently none of our associates are represented by a union (for more information, refer to Item 1A “Risk Factors” of Part I of this Annual Report).

We look at a variety of measures and objectives related to the attraction, development, engagement, safety, and retention of our employees, including:

•Store Staffing. In order to provide the level of customer service that we expect, it is important that we adequately staff our stores with trained employees. As of December 28, 2023, the majority of our stores were staffed at a level that we deem appropriate.

•Training. Training associates is also important to ensuring appropriate levels of customer service. We have a Learning Department, and in 2023, associates engaged in approximately 275,000 hours of training.

•Internal Advancement Opportunities. Our growth opportunities are a critical way to attract and retain employees, and we encourage a promote-from-within environment when internal resources permit. In 2023, approximately 1,550 employees were promoted to more senior positions.

•Culture. We are mindful of the benefits of diversity and associate engagement in all aspects of the employment cycle as they are key to our culture and long-term success. We seek to build a diverse and inclusive workplace where we can leverage our collective talents, striving to ensure that all associates are treated with dignity and respect.

•Safety. Maintaining a safe shopping environment is very important to us. Our Safety & Loss Prevention team works closely with our Store Operations team on safety training and initiatives.

•Rewards. We reward our associates for their hard work on behalf of Floor & Decor and provide a variety of incentives to allow associates to share in the Company’s success, including (i) incentive compensation plans for all associates, (ii) a 401(k) plan with Company-sponsored match, (iii) health care benefits for full-time associates, (iv) an employee stock purchase plan that facilitates purchases of Company stock at a discount by eligible associates, and (v) other benefits such as an employee assistance program.

Government Regulation

We are subject to extensive and varied federal, state and local laws and regulations that impact us, our operations, properties, and suppliers, including those relating to employment, the environment, protection of natural resources, import and export, advertising, labeling, public health and safety, product safety, zoning, and fire codes. We operate our business in accordance with standards and procedures designed to comply with applicable laws and regulations. Compliance with these laws and regulations has not historically had a material effect on our capital expenditures, earnings, competitive position, financial condition, or operating results; however, the effect of compliance in the future cannot be predicted.

Trademarks and other Intellectual Property

As of February 22, 2024, we have 68 registered marks and several pending trademark applications in the United States. We regard our intellectual property, including our over 50 proprietary brands, as having significant value, and our brand is an important factor in the marketing of our products. Accordingly, we have taken, and continue to take, appropriate steps to protect our intellectual property.

Seasonality

Historically, our business has had very little seasonality. Our specialty hard surface flooring and decorative home product offering makes us less susceptible to holiday shopping seasonal patterns compared to other retailers.

Available Information

We maintain a website at www.FloorandDecor.com. The information on or available through our website is not, and should not be considered, a part of this Annual Report. You may access our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports, as well as other reports relating to us that are filed with, or furnished to, the SEC free of charge on our website as soon as reasonably practicable after such material is electronically filed with, or furnished to, the SEC.

ITEM 1A. RISK FACTORS.

You should carefully consider the risks described below, together with all of the other information included in this Annual Report, including our consolidated financial statements and the related notes thereto, before making an investment decision. The risks and uncertainties set out below are not the only risks we face. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial also may materially and adversely affect our business, financial condition, and operating results. If any of the following events occur, our business, financial condition, and operating results could be materially and adversely affected. In that case, the trading price of our common stock could decline, and you may lose all or part of your investment.

Risks Related to Our Business

Declines in certain economic conditions, which impact consumer discretionary spending, could adversely affect our business, financial condition and results of operations.

Consumer discretionary spending affects our sales and is impacted by factors outside of our control, including general economic and political conditions, interest rates, the residential housing market, unemployment rates and wage levels, inflation, disposable income levels, consumer confidence, recession fears, energy costs, consumer credit availability and terms, consumer debt levels, salaries and wage rates, geopolitical events and uncertainty. Declines in the level of consumer confidence and spending and rising interest rates have adversely affected, and could continue to adversely affect, consumer spending habits and consumer discretionary spending, which have resulted in, and may continue to result in, reduced demand for our products.

The hard surface flooring industry is highly dependent on existing home sales because homeowners often replace flooring before selling a home or shortly after purchasing a home and, to a lesser extent, new home construction. In response to increasing inflation, the U.S. Federal Reserve began to raise interest rates in March 2022 and continued to do so through July 2023, contributing to negative existing home sales for over two years. We believe such inflationary pressure has impacted consumer behavior during 2023, particularly in the U.S. housing market and as a result of elevated mortgage rates and higher home prices. Rising interest rates and any such shift in consumer behavior may adversely affect the demand for existing homes, remodeling, and new home construction. In addition, existing home sales, remodeling, and new home construction depend on a number of other factors that are beyond our control, including inflation, tax policy, trade policy, employment levels, consumer confidence, credit availability, real estate prices, home-price appreciation, existing home sales, demographic trends, weather conditions, natural disasters, geopolitical or public safety conditions and general economic conditions. In particular: interest rates and inflation could continue to rise or remain at high levels, undermining consumer confidence and eroding discretionary income; home-price appreciation could slow or turn negative; and regions where we have stores could be impacted by hurricane, fire, or other natural disasters (including those due to the effects of climate change such as increased storm severity, drought, wildfires, and potential flooding due to rising sea levels and storm surges).

We believe any one or a combination of these factors has resulted, and could continue to result in, decreased demand for our products, reduced spending on homebuilding or remodeling of existing homes or caused purchases of new and existing homes to decline. While the vast majority of our net sales are derived from home remodeling activity as opposed to new home construction, the decrease in these areas has adversely affected and could continue to adversely affect our business, financial condition, and operating results.

If we fail to successfully manage the challenges that our planned new store growth poses or encounter unexpected difficulties or higher costs during our expansion, our operating results and future growth opportunities could be adversely affected.

We have 221 warehouse-format stores and five small-format standalone design studios located throughout the United States as of December 28, 2023. We plan to continue opening new stores for the next several years. This growth strategy and the investment associated with the development of each new store may cause our operating results to fluctuate and be unpredictable or decrease our profits. We cannot ensure that store locations will be available to us, or that they will be available on terms acceptable to us. If additional retail store locations are unavailable on acceptable terms, we may not be able to carry out a significant part of our growth strategy or our new stores’ profitability may be lower. Certain of our new store openings are expected to be smaller stores in smaller markets. We have limited experience executing this strategy, and we cannot guarantee that we will be successful in this strategy. Our future operating results and ability to grow will depend on various other factors, including our ability to: successfully select new markets and store locations; attract, train and retain highly qualified managers and staff; maintain our reputation of providing quality, safe and compliant products; and manage store opening costs, including rising construction costs and costs due to delays in obtaining necessary permits and completing construction.

In addition, stores opened in new markets have had, and many continue to have, higher construction, occupancy and operating costs than stores opened in the past, and such stores may have lower profitability than stores opened in the past. In addition, laws or regulations in these new markets may make opening new stores more difficult or cause unexpected delays. For example, we have experienced unexpected delays in opening new stores due to delays in obtaining necessary construction and occupancy permits, which have resulted in higher costs than previously anticipated. As we continue to open new stores, the ultimate cost of future store openings could continue to rise significantly due to construction-related or other reasons, including construction and other delays and cost overruns, such as shortages of materials, shortages of skilled labor or work stoppages, unforeseen construction, scheduling, engineering, environmental or geological problems, governmental or permitting delays, weather interference, fires or other casualty losses and unanticipated cost increases. We cannot guarantee that any project will be completed on time, and delays in store openings have had, and may continue to have, a negative impact on our business and operating results. In addition, consumers in new markets may be less familiar with our brand, and we may need to increase brand awareness in such markets through additional investments in advertising or high cost locations with more prominent visibility.

As a result of these factors and other factors that may be outside of our control, newly opened stores may not succeed or may reach profitability at all, or may be slower to reach profitability than we expect. Future markets and newly opened stores may not be successful and, even if they are successful, our comparable store sales may not increase at historical rates or may decrease. To the extent that we are not able to overcome these various challenges, our operating results and future growth opportunities could be adversely affected. Furthermore, we may incur costs associated with the closure of underperforming stores, and such store closures may adversely impact our revenues.

If we are unable to enter into leases for additional stores on acceptable terms or renew or replace our current store leases, or if one or more of our current leases is terminated prior to expiration of its stated term and we cannot find suitable alternate locations, our growth and profitability could be adversely affected.

We currently lease the majority of our store locations and our store support center. Our growth strategy largely depends on our ability to identify and open future store locations, which can be difficult because our warehouse-format stores in major metropolitan markets generally require at least 60,000 square feet of floor space. Our ability to negotiate acceptable lease terms for these store locations, to re-negotiate acceptable terms on expiring leases or to negotiate acceptable terms for suitable alternate locations depends on conditions in the real estate market, competition for desirable properties, our relationships with current and prospective landlords, and on other factors that are not within our control. We also intend to purchase the real property for a small number of new locations, and such strategy may not be successful. Any or all of these factors and conditions could adversely affect our growth and profitability.

Any failure by us to successfully anticipate trends may lead to loss of consumer acceptance of our products, resulting in reduced net sales.

Each of our stores is stocked with a localized product mix based on consumer demands in a particular market. Our success depends on our ability to anticipate and respond to changing trends and consumer demands in these markets in a timely manner. Our ability to accurately forecast demand for our products could be affected by many factors. If we fail to identify and respond to emerging trends, consumer acceptance of our merchandise and our image with current or potential customers may be harmed, which could reduce our net sales. Additionally, if we misjudge market trends, we may significantly overstock unpopular products, incur excess inventory costs and be forced to reduce the sales price of such products or incur inventory write-downs, which would adversely affect our operating results. Conversely, shortages of products that prove popular could also reduce our net sales through missed sales and a loss of customer loyalty.